CATEGORY

CATEGORY

CATEGORY

News

News

News

What New Flexible Plastic Regulations Mean for rPET, rHDPE, rLDPE, and rPP Demand

What New Flexible Plastic Regulations Mean for rPET, rHDPE, rLDPE, and rPP Demand

What New Flexible Plastic Regulations Mean for rPET, rHDPE, rLDPE, and rPP Demand

New EU, UK, and California regulations are pushing recycled content into PE and PP streams, not just PET. Here's what rising demand for rPET, rHDPE, rLDPE, and rPP means for PCR buyers and sellers.

Regulatory Pressure Is Rising

Reuters reported that regulatory pressure on flexible plastic packaging is rising across major markets. In the EU, most flexible plastic packaging sold by 2030 will need to meet minimum recycled-content thresholds, including at least 10% for non-PET packaging and 35% for other plastic packaging categories. By 2035, companies will also need to prove that their packaging is being recycled at scale, which means the full value chain — collection, sorting, recycling capacity, and end markets — must exist in practice, not just in policy language.

That matters because flexible plastics remain one of the hardest packaging formats to recycle. Reuters cited Pew Charitable Trusts data showing that flexible and multilayer plastics account for 58% of global plastic packaging but are recycled through formal systems at less than 4%, while also making up 80% of plastic leakage into the ocean. The structural problem is clear: brands favor flexible packaging because it is light and cost-efficient, but its multilayer design and food contamination make conventional mechanical recycling difficult.

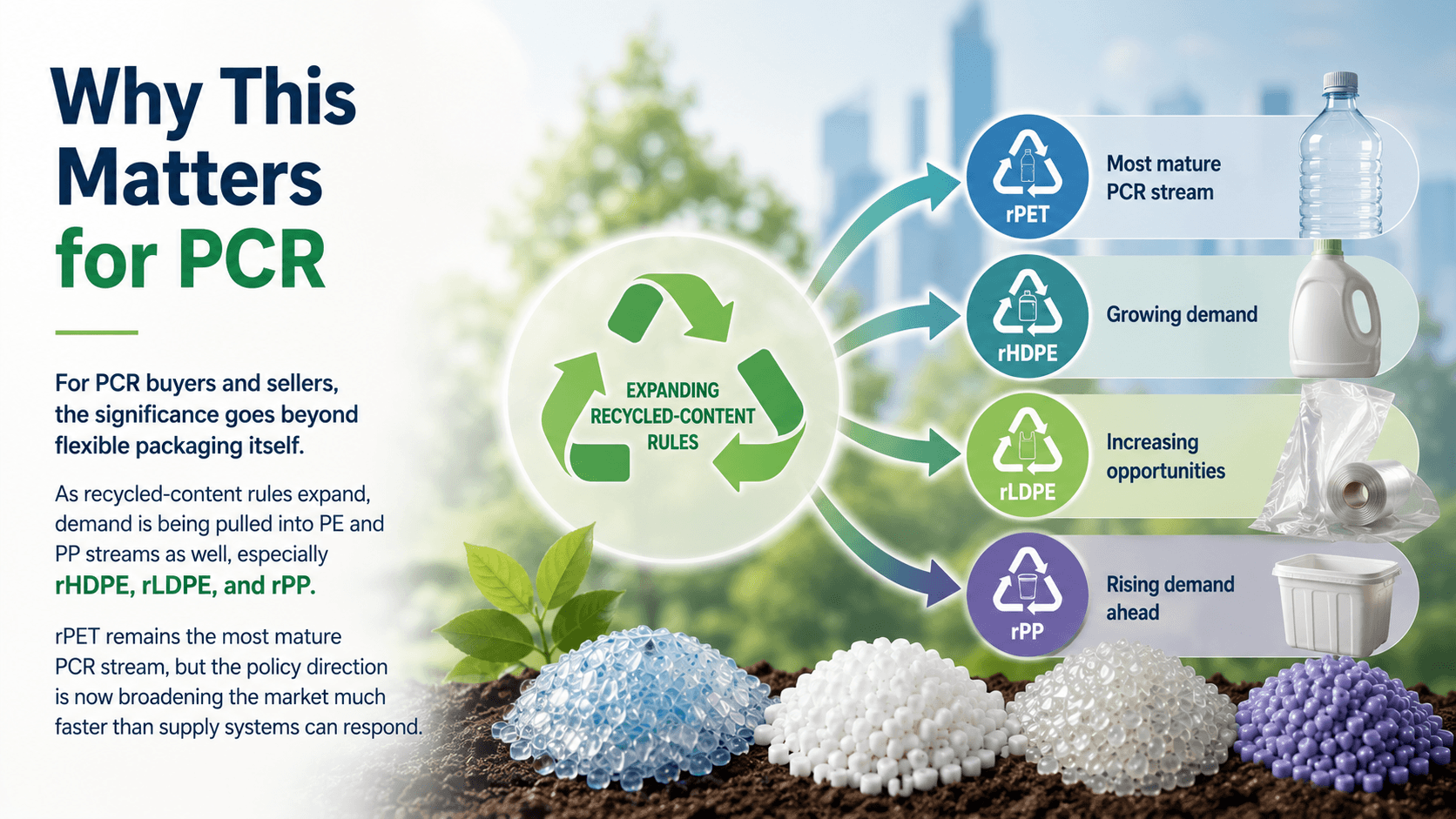

Why This Matters for PCR

For PCR buyers and sellers, the significance goes beyond flexible packaging itself. As recycled-content rules expand, demand is being pulled into PE and PP streams as well, especially rHDPE, rLDPE, and rPP. rPET remains the most mature PCR stream, but the policy direction is now broadening the market much faster than supply systems can respond.

Polymer-by-Polymer Impact

rPET

The most mature PCR stream, supported by years of beverage bottle mandates. The latest regulations reinforce this existing market rather than creating it from scratch. Even so, the push toward higher recycled content across more packaging formats is likely to tighten quality expectations — particularly around color, consistency, and food-contact performance.

rHDPE & rLDPE

More directly affected by flexible film collection rules. These streams could benefit from a larger future feedstock base if collection and sorting infrastructure improves — but the near-term picture remains uneven. In many regions, collection systems are not yet mature enough to deliver consistent volumes, meaning buyers may continue to face limited supply and irregular quality.

rPP

Often overlooked in flexible packaging discussions, but gaining importance. PP films and rigid PP containers face many of the same contamination and multilayer challenges as PE-based formats. As chemical recycling and dissolution-based technologies improve, rPP may become a more attractive option over the next several years — particularly for non-food applications.

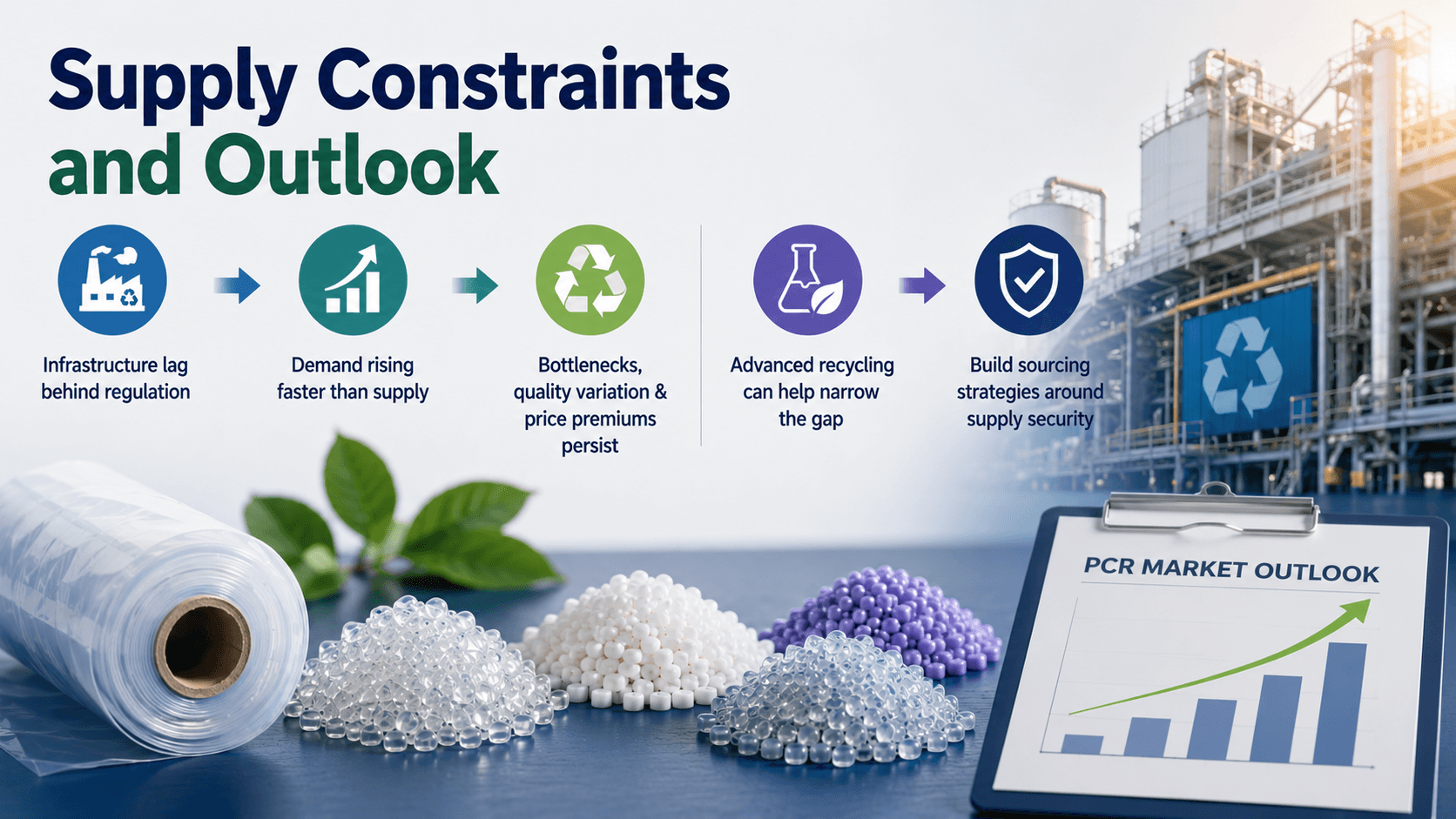

Supply Constraints and Outlook

For buyers, the biggest issue is still infrastructure lag. Regulation is moving faster than recycling capacity, and that mismatch is creating a market where demand is rising faster than supply can respond. This is why bottlenecks, quality variation, and price premiums are likely to remain part of the PCR market in the near term.

Chemical recycling and dissolution-based PCR may help narrow the gap, but they are not likely to solve it quickly. These processes still carry higher production costs, and in many cases they depend on new investment, technical validati on, and stable offtake demand. That means buyers should expect price premiums to persist and should build sourcing strategies around supply security rather than assuming rapid price convergence with virgin material.

The Strategic Takeaway

The key takeaway is simple: this is not a 2030 issue. PCR sourcing strategies need to change now, because recycled content is becoming a basic condition for competitiveness across the packaging value chain.

Image generated with ChatGPT

Source

Reuters, "Plastic bags, wraps and pouches face short shelf life" → Read the Source

Posted by Regenport

Regenport is a global platform connecting buyers and suppliers in the recycled materials and sustainable packaging industries.

Regulatory Pressure Is Rising

Reuters reported that regulatory pressure on flexible plastic packaging is rising across major markets. In the EU, most flexible plastic packaging sold by 2030 will need to meet minimum recycled-content thresholds, including at least 10% for non-PET packaging and 35% for other plastic packaging categories. By 2035, companies will also need to prove that their packaging is being recycled at scale, which means the full value chain — collection, sorting, recycling capacity, and end markets — must exist in practice, not just in policy language.

That matters because flexible plastics remain one of the hardest packaging formats to recycle. Reuters cited Pew Charitable Trusts data showing that flexible and multilayer plastics account for 58% of global plastic packaging but are recycled through formal systems at less than 4%, while also making up 80% of plastic leakage into the ocean. The structural problem is clear: brands favor flexible packaging because it is light and cost-efficient, but its multilayer design and food contamination make conventional mechanical recycling difficult.

Why This Matters for PCR

For PCR buyers and sellers, the significance goes beyond flexible packaging itself. As recycled-content rules expand, demand is being pulled into PE and PP streams as well, especially rHDPE, rLDPE, and rPP. rPET remains the most mature PCR stream, but the policy direction is now broadening the market much faster than supply systems can respond.

Polymer-by-Polymer Impact

rPET

The most mature PCR stream, supported by years of beverage bottle mandates. The latest regulations reinforce this existing market rather than creating it from scratch. Even so, the push toward higher recycled content across more packaging formats is likely to tighten quality expectations — particularly around color, consistency, and food-contact performance.

rHDPE & rLDPE

More directly affected by flexible film collection rules. These streams could benefit from a larger future feedstock base if collection and sorting infrastructure improves — but the near-term picture remains uneven. In many regions, collection systems are not yet mature enough to deliver consistent volumes, meaning buyers may continue to face limited supply and irregular quality.

rPP

Often overlooked in flexible packaging discussions, but gaining importance. PP films and rigid PP containers face many of the same contamination and multilayer challenges as PE-based formats. As chemical recycling and dissolution-based technologies improve, rPP may become a more attractive option over the next several years — particularly for non-food applications.

Supply Constraints and Outlook

For buyers, the biggest issue is still infrastructure lag. Regulation is moving faster than recycling capacity, and that mismatch is creating a market where demand is rising faster than supply can respond. This is why bottlenecks, quality variation, and price premiums are likely to remain part of the PCR market in the near term.

Chemical recycling and dissolution-based PCR may help narrow the gap, but they are not likely to solve it quickly. These processes still carry higher production costs, and in many cases they depend on new investment, technical validati on, and stable offtake demand. That means buyers should expect price premiums to persist and should build sourcing strategies around supply security rather than assuming rapid price convergence with virgin material.

The Strategic Takeaway

The key takeaway is simple: this is not a 2030 issue. PCR sourcing strategies need to change now, because recycled content is becoming a basic condition for competitiveness across the packaging value chain.

Image generated with ChatGPT

Source

Reuters, "Plastic bags, wraps and pouches face short shelf life" → Read the Source

Posted by Regenport

Regenport is a global platform connecting buyers and suppliers in the recycled materials and sustainable packaging industries.