CATEGORY

CATEGORY

CATEGORY

Trend

Trend

Trend

June 2026 Recycled Plastics Market Review: Weak Trend with Emerging Regional Opportunities

June 2026 Recycled Plastics Market Review: Weak Trend with Emerging Regional Opportunities

June 2026 Recycled Plastics Market Review: Weak Trend with Emerging Regional Opportunities

The recycled plastics market in June 2026 remained under pressure due to falling virgin polymer prices and rising logistics costs. However, regulatory shifts and regional supply dynamics revealed selective opportunities across rPET, rHDPE, and other recycled polymers.

Market Overview: Continued Weakness in June

The global recycled plastics market in June 2026 maintained a generally weak trajectory. Despite this, market behavior was far from uniform, with clear differentiation emerging across regions and product segments.

While overall demand softened, certain niches demonstrated resilience, indicating that the market is no longer moving in a single unified direction.

Virgin Polymer Price Decline and Demand Pressure

One of the most significant drivers was the continued decline in virgin polymer prices. As prices for primary resins dropped, the cost competitiveness of recycled materials weakened considerably.

Buyers responded by adopting a cautious stance, delaying purchases and prioritizing short-term flexibility over long-term procurement. This resulted in reduced transaction volumes across multiple recycled polymer grades.

Logistics Costs and Trade Flow Constraints

Rising ocean freight rates from Asia added another layer of complexity. For supply chains dependent on long-distance sourcing, increased transportation costs placed additional pressure on margins.

As a result, cross-regional trade flows became less attractive, reinforcing a shift toward localized sourcing strategies.

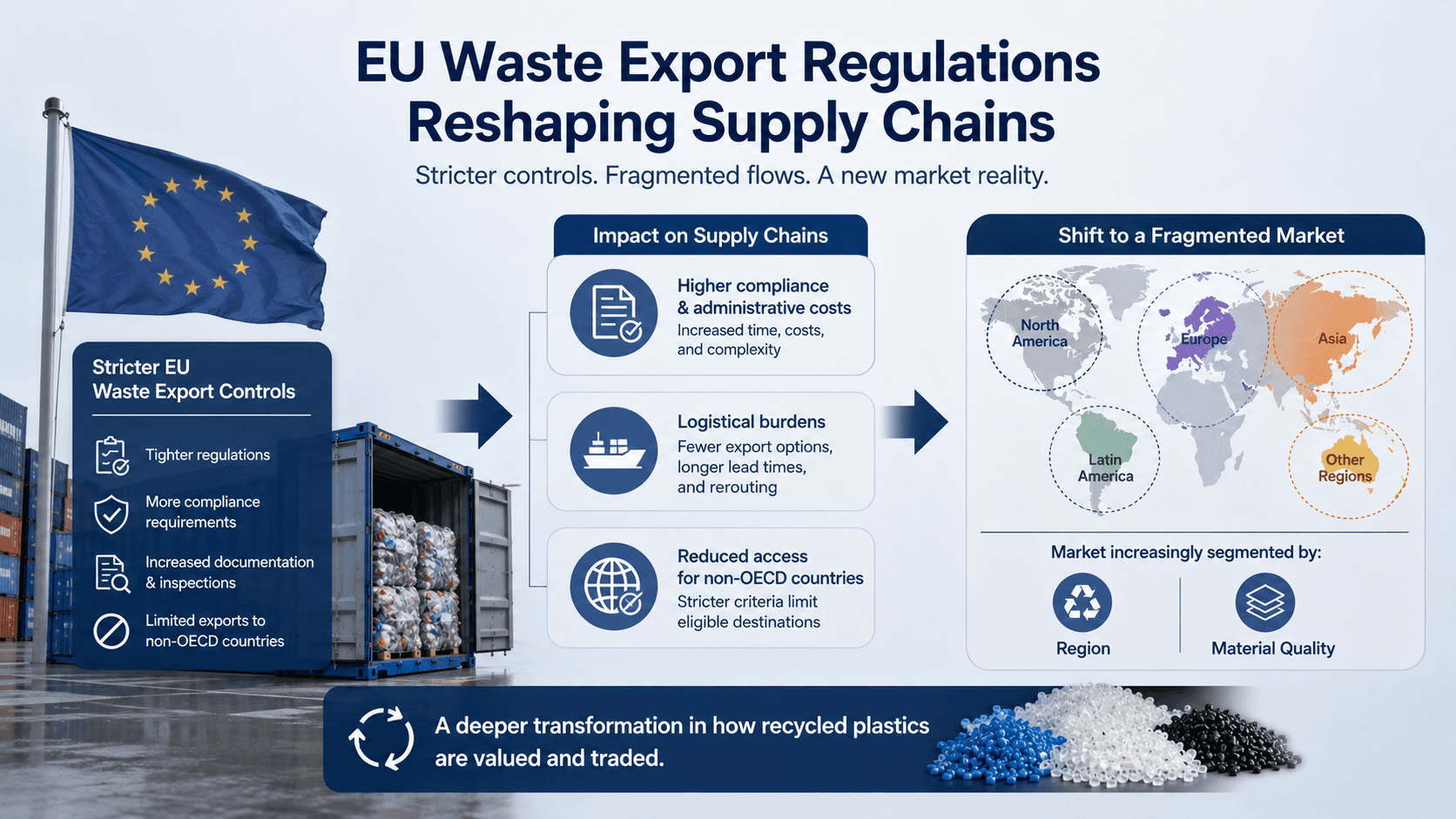

EU Waste Export Regulations Reshaping Supply Chains

Regulatory developments, particularly stricter EU waste export controls, introduced new structural changes to the market.

Increased compliance requirements and logistical burdens for non-OECD imports led to fragmentation in supply chains. The market is increasingly segmented by region and material quality, rather than operating as a globally fluid system.

This shift signals a deeper transformation in how recycled plastics are valued and traded.

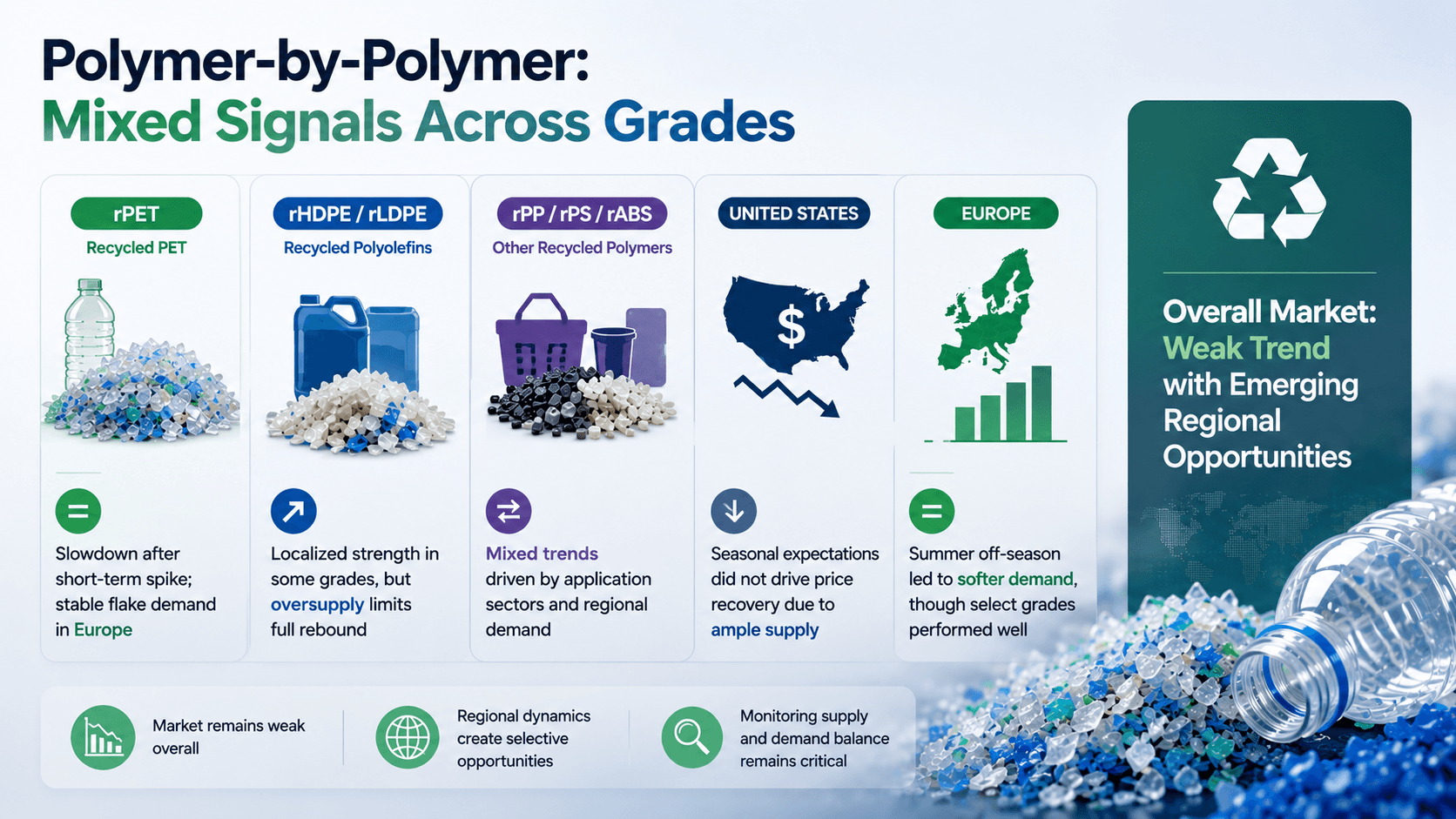

Polymer-by-Polymer: Mixed Signals Across Grades

Recycled PET (rPET) experienced a slowdown following a short-term demand spike. However, in Europe, flake demand remained relatively stable compared to other segments.

In the United States, seasonal expectations did not translate into strong price recovery due to sufficient supply availability.

Recycled polyolefins such as rHDPE and rLDPE showed localized strength in certain grades, driven by higher production costs and supply constraints. Nevertheless, broader oversupply conditions prevented a full market rebound.

Other recycled polymers, including rPP, rPS, and rABS, displayed mixed trends depending on application sectors and regional demand.

In Europe, the onset of the summer off-season led to softer demand overall, although select grades continued to perform relatively well.

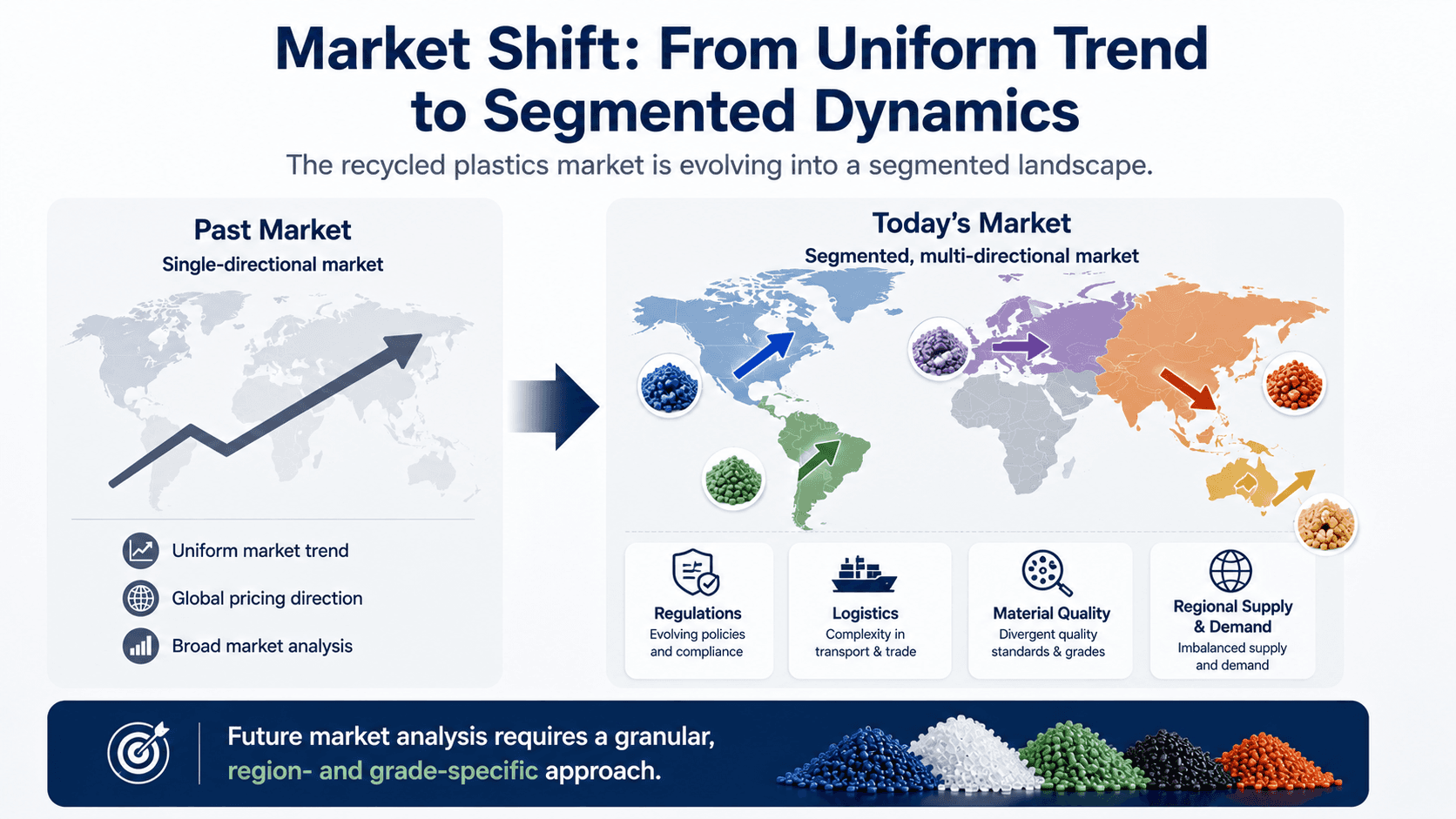

Market Shift: From Uniform Trend to Segmented Dynamics

The key takeaway from June is clear. The recycled plastics market is no longer a single-directional market.

Instead, it is evolving into a segmented landscape shaped by regulations, logistics, material quality, and regional supply-demand balances. Future market analysis will require a more granular approach, focusing on specific regions and grades rather than broad market direction.

Conclusion Insight

In summary, June 2026 marked a transitional period for the recycled plastics market—characterized by overall weakness but also the emergence of selective opportunities driven by structural changes.

Market Overview: Continued Weakness in June

The global recycled plastics market in June 2026 maintained a generally weak trajectory. Despite this, market behavior was far from uniform, with clear differentiation emerging across regions and product segments.

While overall demand softened, certain niches demonstrated resilience, indicating that the market is no longer moving in a single unified direction.

Virgin Polymer Price Decline and Demand Pressure

One of the most significant drivers was the continued decline in virgin polymer prices. As prices for primary resins dropped, the cost competitiveness of recycled materials weakened considerably.

Buyers responded by adopting a cautious stance, delaying purchases and prioritizing short-term flexibility over long-term procurement. This resulted in reduced transaction volumes across multiple recycled polymer grades.

Logistics Costs and Trade Flow Constraints

Rising ocean freight rates from Asia added another layer of complexity. For supply chains dependent on long-distance sourcing, increased transportation costs placed additional pressure on margins.

As a result, cross-regional trade flows became less attractive, reinforcing a shift toward localized sourcing strategies.

EU Waste Export Regulations Reshaping Supply Chains

Regulatory developments, particularly stricter EU waste export controls, introduced new structural changes to the market.

Increased compliance requirements and logistical burdens for non-OECD imports led to fragmentation in supply chains. The market is increasingly segmented by region and material quality, rather than operating as a globally fluid system.

This shift signals a deeper transformation in how recycled plastics are valued and traded.

Polymer-by-Polymer: Mixed Signals Across Grades

Recycled PET (rPET) experienced a slowdown following a short-term demand spike. However, in Europe, flake demand remained relatively stable compared to other segments.

In the United States, seasonal expectations did not translate into strong price recovery due to sufficient supply availability.

Recycled polyolefins such as rHDPE and rLDPE showed localized strength in certain grades, driven by higher production costs and supply constraints. Nevertheless, broader oversupply conditions prevented a full market rebound.

Other recycled polymers, including rPP, rPS, and rABS, displayed mixed trends depending on application sectors and regional demand.

In Europe, the onset of the summer off-season led to softer demand overall, although select grades continued to perform relatively well.

Market Shift: From Uniform Trend to Segmented Dynamics

The key takeaway from June is clear. The recycled plastics market is no longer a single-directional market.

Instead, it is evolving into a segmented landscape shaped by regulations, logistics, material quality, and regional supply-demand balances. Future market analysis will require a more granular approach, focusing on specific regions and grades rather than broad market direction.

Conclusion Insight

In summary, June 2026 marked a transitional period for the recycled plastics market—characterized by overall weakness but also the emergence of selective opportunities driven by structural changes.