CATEGORY

CATEGORY

CATEGORY

Trend

Trend

Trend

Virgin Price Collapse Drives Recycled Polymer Market Divergence – Week 1, July

Virgin Price Collapse Drives Recycled Polymer Market Divergence – Week 1, July

Virgin Price Collapse Drives Recycled Polymer Market Divergence – Week 1, July

Virgin PVC/PE/PP prices fell sharply this week, while European R-HDPE/R-PP recyclers held prices firm on strong bale costs. With buyers in hand-to-mouth mode and seasonal demand weak, grade-by-grade divergence is expected to persist through late July.

The recycled polymer market is currently being pulled in three different directions. While virgin polymer prices continue to decline toward pre-war levels following the Middle East ceasefire, recyclers in Europe are maintaining firm pricing due to strong feedstock costs. At the same time, buyers across both Europe and the US are adopting a cautious, hand-to-mouth purchasing strategy amid ongoing uncertainty.

Three Key Drivers Behind Current Market Pressure

Virgin Prices Continue to Slide Toward Pre-War Levels

The ceasefire in the Middle East has had a major impact on the entire value chain. European feedstock costs, including ethylene, settled at EUR 1,445/mt in June and have since moved down toward EUR 1,200/mt, while US spot PVC prices have fallen to their lowest level since the conflict began. As virgin material prices drop, the price premium for recycled products has largely disappeared, pushing buyers into a wait-and-see mode. Many are uncertain how much further virgin prices could fall in the coming weeks.Feedstock Costs Are Not Falling as Fast as End-Product Prices

In Europe, recyclers producing rHDPE and rPP have been relatively resilient against the virgin downtrend, supported by strong demand for post-consumer bales. The price spread between natural rHDPE pellets and virgin HDPE has widened again this week, indicating that European recyclers are still able to defend their pricing despite the broader market decline.Seasonal Demand Weakness

With plastic converters in Europe and the US preparing for seasonal shutdowns, particularly in August, demand for recycled grades has weakened significantly. Buying appetite across rHDPE, rPP, and other recycled polymer categories is currently at a low point, adding further pressure to the market.

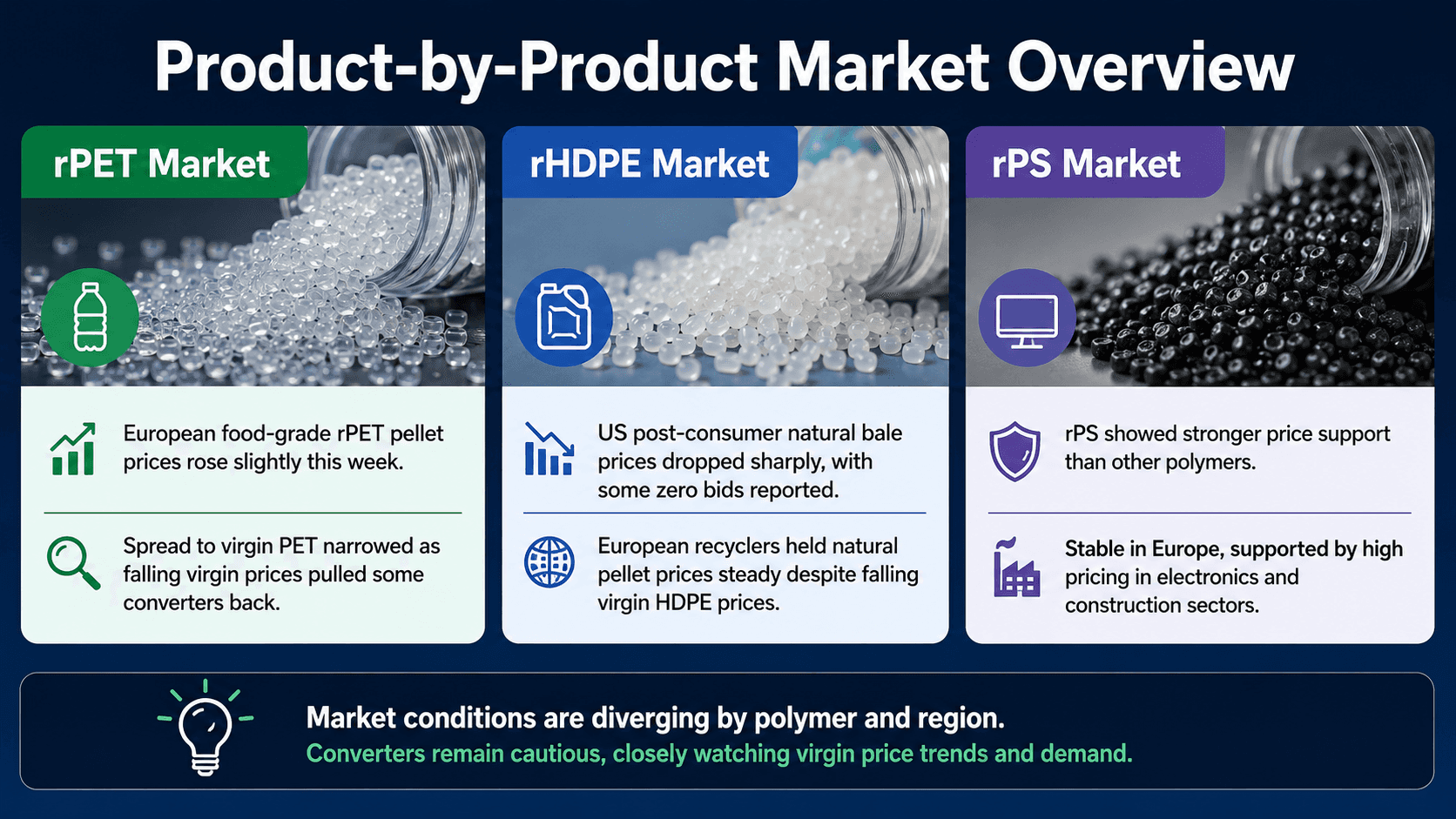

Product-by-Product Market Overview

rPET Market

European food-grade rPET pellets saw a slight price increase this week, although the spread to virgin PET narrowed further as falling virgin prices pulled some converters back toward virgin material. The overall trend remains cautious, with converters closely watching whether virgin PET prices will stabilize or continue to decline.

rHDPE Market

The US market experienced the most dramatic move: post-consumer natural bale prices dropped sharply, with some recyclers reporting zero bids for bales. In contrast, European recyclers largely held natural pellet prices steady despite the sharp selloff in virgin HDPE, reflecting the divergence in feedstock dynamics between the two regions.

rPS Market

Recycled polystyrene showed stronger price support compared to other polymer categories. In Europe, black rPS pellet prices remained stable, supported by relatively high pricing in the electronics and construction sectors, where production and energy costs continue to be elevated.

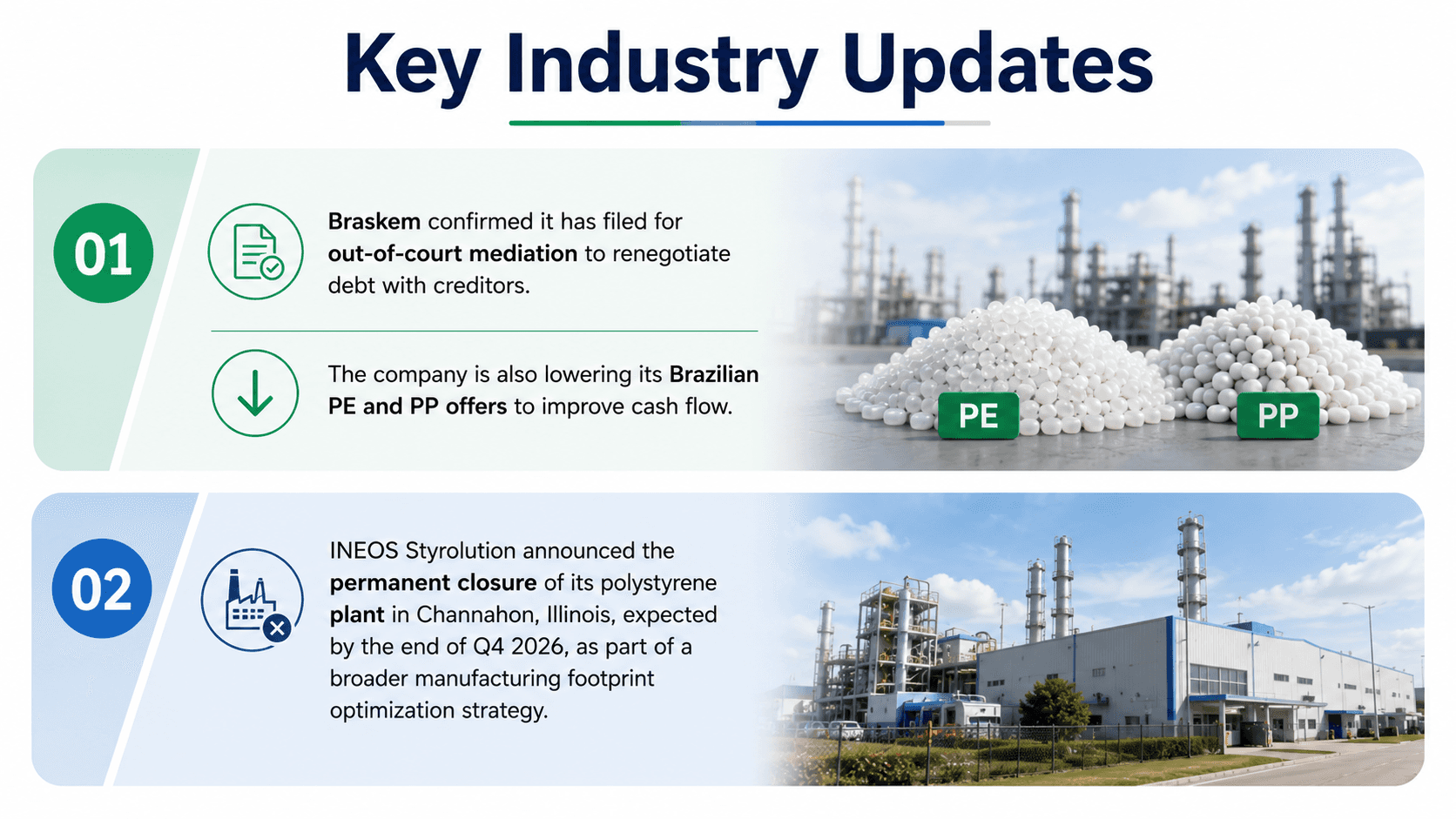

Key Industry Updates

Braskem confirmed it has filed for out-of-court mediation to renegotiate debt with creditors. The company is also lowering its Brazilian PE and PP offers to improve cash flow.

INEOS Styrolution announced the permanent closure of its polystyrene plant in Channahon, Illinois, expected by the end of Q4 2026, as part of a broader manufacturing footprint optimization strategy.

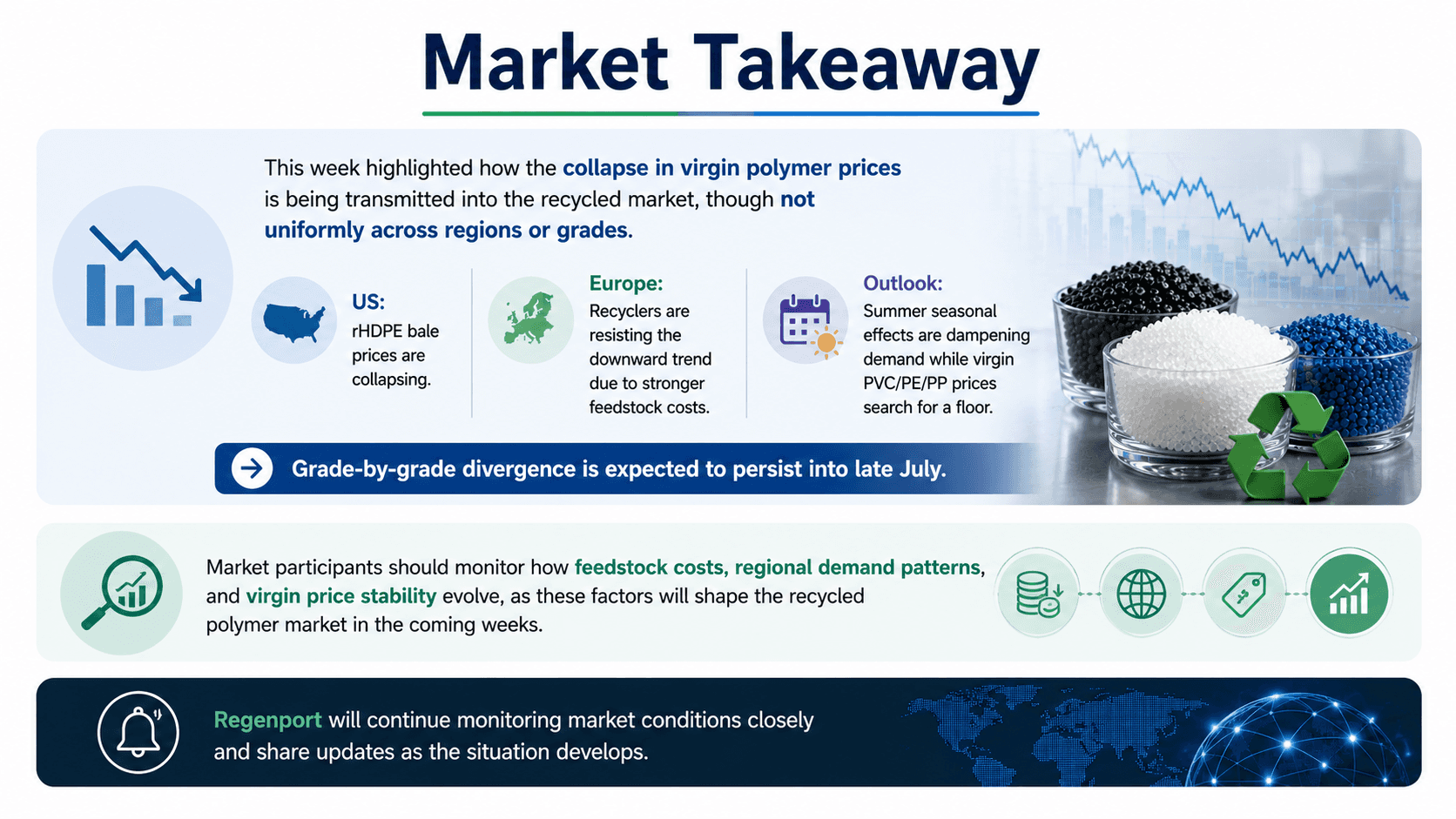

Market Takeaway

This week highlighted how the collapse in virgin polymer prices is being transmitted into the recycled market, though not uniformly across regions or grades. In the US, rHDPE bale prices are collapsing, while in Europe, recyclers are resisting the downward trend due to stronger feedstock costs. As summer seasonal effects further dampen demand and virgin PVC/PE/PP prices continue searching for a floor, this grade-by-grade divergence is expected to persist into late July.

Market participants should monitor how feedstock costs, regional demand patterns, and virgin price stability evolve, as these factors will shape the recycled polymer market in the coming weeks. Regenport will continue monitoring market conditions closely and share updates as the situation develops.

Image generated with ChatGPT

Posted by Regenport

Regenport is a global platform connecting buyers and suppliers in the recycled materials and sustainable packaging industries.

The recycled polymer market is currently being pulled in three different directions. While virgin polymer prices continue to decline toward pre-war levels following the Middle East ceasefire, recyclers in Europe are maintaining firm pricing due to strong feedstock costs. At the same time, buyers across both Europe and the US are adopting a cautious, hand-to-mouth purchasing strategy amid ongoing uncertainty.

Three Key Drivers Behind Current Market Pressure

Virgin Prices Continue to Slide Toward Pre-War Levels

The ceasefire in the Middle East has had a major impact on the entire value chain. European feedstock costs, including ethylene, settled at EUR 1,445/mt in June and have since moved down toward EUR 1,200/mt, while US spot PVC prices have fallen to their lowest level since the conflict began. As virgin material prices drop, the price premium for recycled products has largely disappeared, pushing buyers into a wait-and-see mode. Many are uncertain how much further virgin prices could fall in the coming weeks.Feedstock Costs Are Not Falling as Fast as End-Product Prices

In Europe, recyclers producing rHDPE and rPP have been relatively resilient against the virgin downtrend, supported by strong demand for post-consumer bales. The price spread between natural rHDPE pellets and virgin HDPE has widened again this week, indicating that European recyclers are still able to defend their pricing despite the broader market decline.Seasonal Demand Weakness

With plastic converters in Europe and the US preparing for seasonal shutdowns, particularly in August, demand for recycled grades has weakened significantly. Buying appetite across rHDPE, rPP, and other recycled polymer categories is currently at a low point, adding further pressure to the market.

Product-by-Product Market Overview

rPET Market

European food-grade rPET pellets saw a slight price increase this week, although the spread to virgin PET narrowed further as falling virgin prices pulled some converters back toward virgin material. The overall trend remains cautious, with converters closely watching whether virgin PET prices will stabilize or continue to decline.

rHDPE Market

The US market experienced the most dramatic move: post-consumer natural bale prices dropped sharply, with some recyclers reporting zero bids for bales. In contrast, European recyclers largely held natural pellet prices steady despite the sharp selloff in virgin HDPE, reflecting the divergence in feedstock dynamics between the two regions.

rPS Market

Recycled polystyrene showed stronger price support compared to other polymer categories. In Europe, black rPS pellet prices remained stable, supported by relatively high pricing in the electronics and construction sectors, where production and energy costs continue to be elevated.

Key Industry Updates

Braskem confirmed it has filed for out-of-court mediation to renegotiate debt with creditors. The company is also lowering its Brazilian PE and PP offers to improve cash flow.

INEOS Styrolution announced the permanent closure of its polystyrene plant in Channahon, Illinois, expected by the end of Q4 2026, as part of a broader manufacturing footprint optimization strategy.

Market Takeaway

This week highlighted how the collapse in virgin polymer prices is being transmitted into the recycled market, though not uniformly across regions or grades. In the US, rHDPE bale prices are collapsing, while in Europe, recyclers are resisting the downward trend due to stronger feedstock costs. As summer seasonal effects further dampen demand and virgin PVC/PE/PP prices continue searching for a floor, this grade-by-grade divergence is expected to persist into late July.

Market participants should monitor how feedstock costs, regional demand patterns, and virgin price stability evolve, as these factors will shape the recycled polymer market in the coming weeks. Regenport will continue monitoring market conditions closely and share updates as the situation develops.

Image generated with ChatGPT

Posted by Regenport

Regenport is a global platform connecting buyers and suppliers in the recycled materials and sustainable packaging industries.