CATEGORY

CATEGORY

Trend

Trend

Recycled Polymer Market Faces Continued Pressure as Virgin Prices Weaken and Freight Costs Rise – Week 4, June 2026

Recycled Polymer Market Faces Continued Pressure as Virgin Prices Weaken and Freight Costs Rise – Week 4, June 2026

The recycled polymer market remained under pressure this week, driven by lower crude oil prices, softer European demand, and higher freight costs. R-PET and R-PP saw the greatest weakness, while white R-PS remained resilient on stronger demand. Market sentiment is expected to stay cautious in the near term.

The recycled polymer market remained under pressure this week, shaped by three converging factors: lower crude oil prices amid US–Iran peace deal expectations, seasonal demand softness in Europe, and rising shipping costs out of Asia. Together, these trends have made buyers more cautious and reduced appetite for recycled feedstock across key grades.

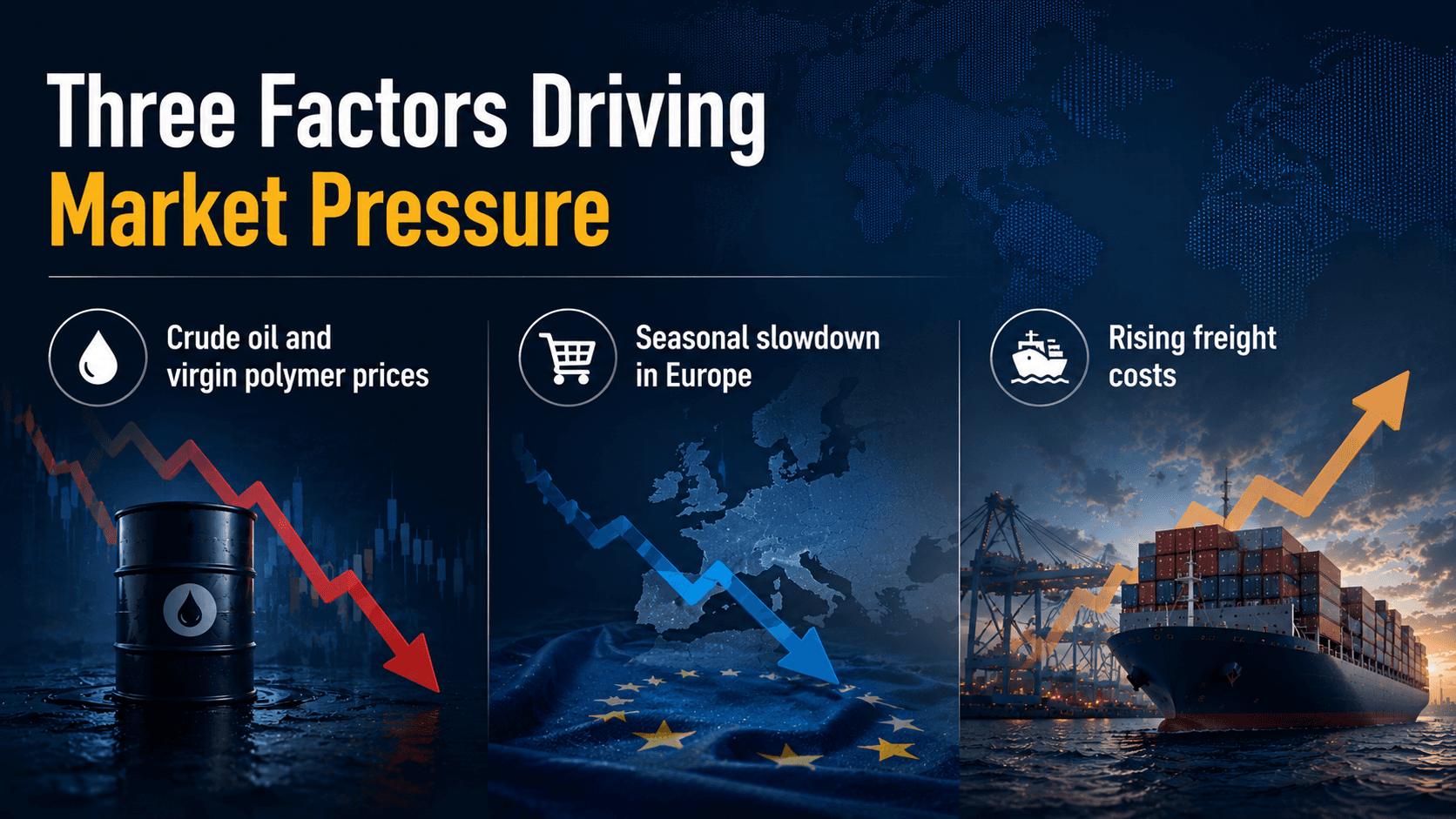

Three Factors Driving Market Pressure

Crude oil and virgin polymer prices

Expectations of a US–Iran peace agreement pushed Brent crude below 80 USD per barrel this week, pulling virgin polymer prices lower in tandem. As the price gap between virgin and recycled materials narrows, some buyers have begun shifting their procurement mix toward virgin feedstock, reducing near-term demand for recycled alternatives.

Seasonal slowdown in Europe

Purchasing activity in Europe is easing as the market approaches the summer holiday period. Export flows from Asia to European converters have also softened, adding to the overall demand slowdown across the region.

Rising freight costs

Shipping rates out of Asia have roughly doubled since April, creating an additional barrier to cross-border cargo movement. For recycled polymer trades that depend on longer supply chains, the economics of importing have become more challenging.

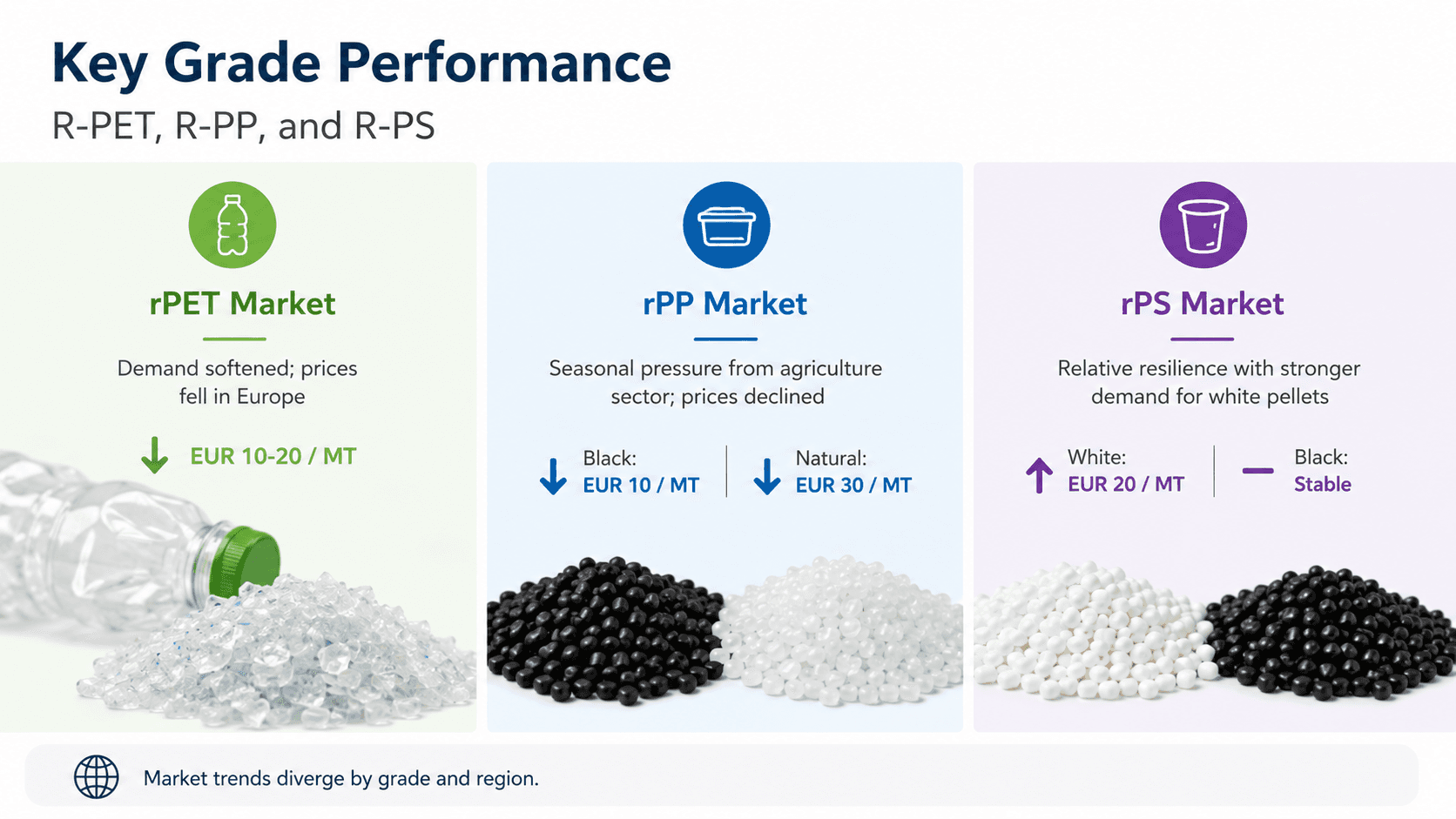

Key Grade Performance: R-PET, R-PP, and R-PS

rPET Market

Demand for R-PET continued to soften this week. Thermoformers and converters have adjusted their procurement mix toward virgin feedstock in some cases, and several recyclers noted that rPET demand has returned to pre-conflict levels — reflecting how much of the recent demand strength was tied to the period of US–Iran tensions.

In Europe, flake and pellet prices fell by EUR 10 to EUR 20 per metric ton. In the United States, overall fundamentals remained sluggish, although bale demand held relatively stable, supported by steady purchases from Mexico.

rPP Market

European R-PP prices came under seasonal pressure as agricultural sector demand moves toward its seasonal close. Black pellets declined by EUR 10 per metric ton, while natural pellets fell by EUR 30 per metric ton.

rPS Market

R-PS showed relative resilience despite the broader pressure from lower virgin prices. White pellet prices rose by EUR 20 per metric ton on stronger demand, while black pellets remained broadly stable — a reminder that grade-specific demand dynamics can diverge meaningfully from the broader market trend.

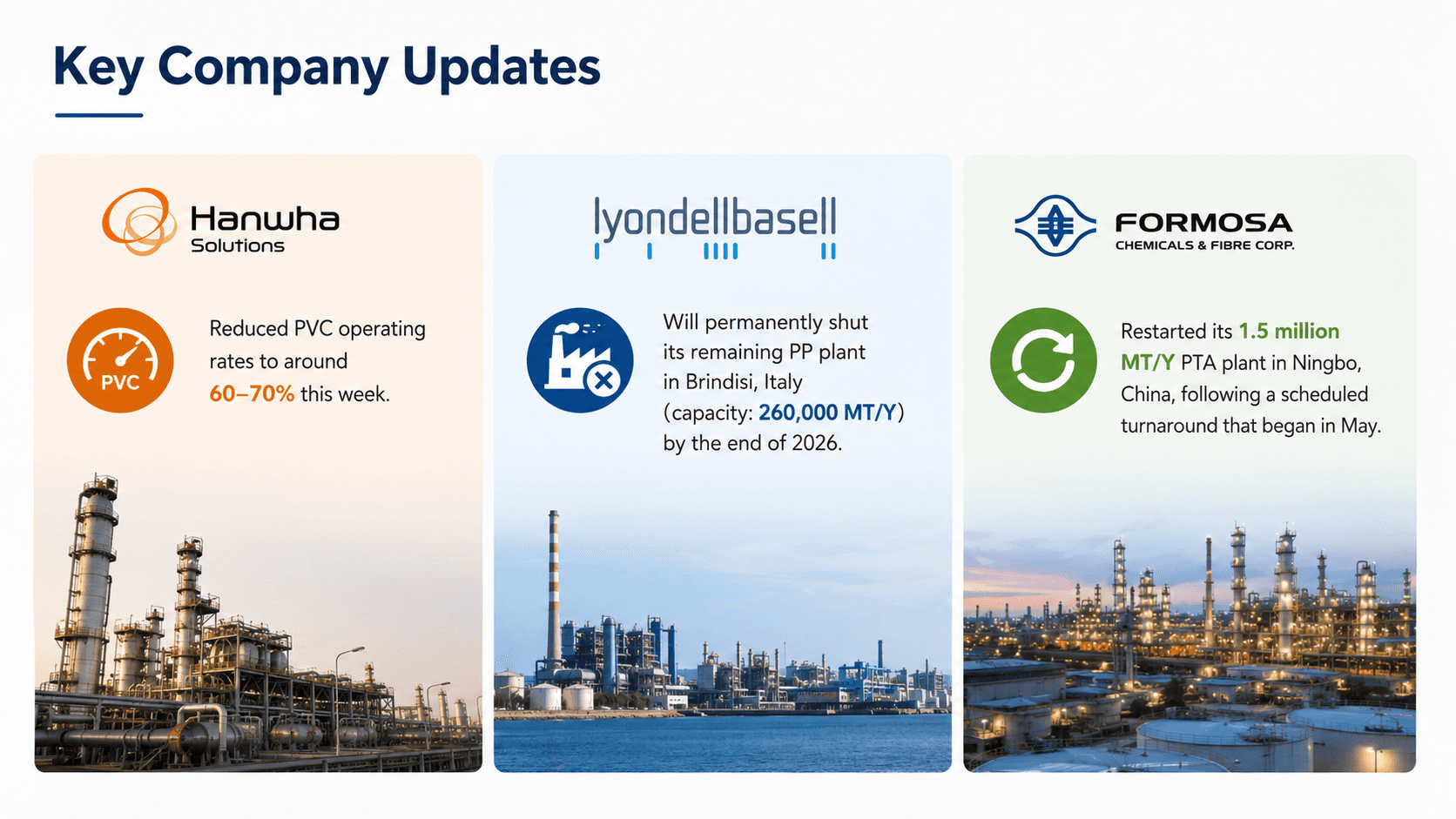

Key company updates

Hanwha Solutions reduced its PVC operating rates to around 60–70% this week. LyondellBasell officially confirmed it will permanently shut its remaining PP plant in Brindisi, Italy — capacity of 260,000 metric tons per year — by the end of 2026. Formosa Chemical & Fibre Corp. restarted its 1.5 million metric ton per year PTA plant in Ningbo, China, following a scheduled turnaround that began in May.

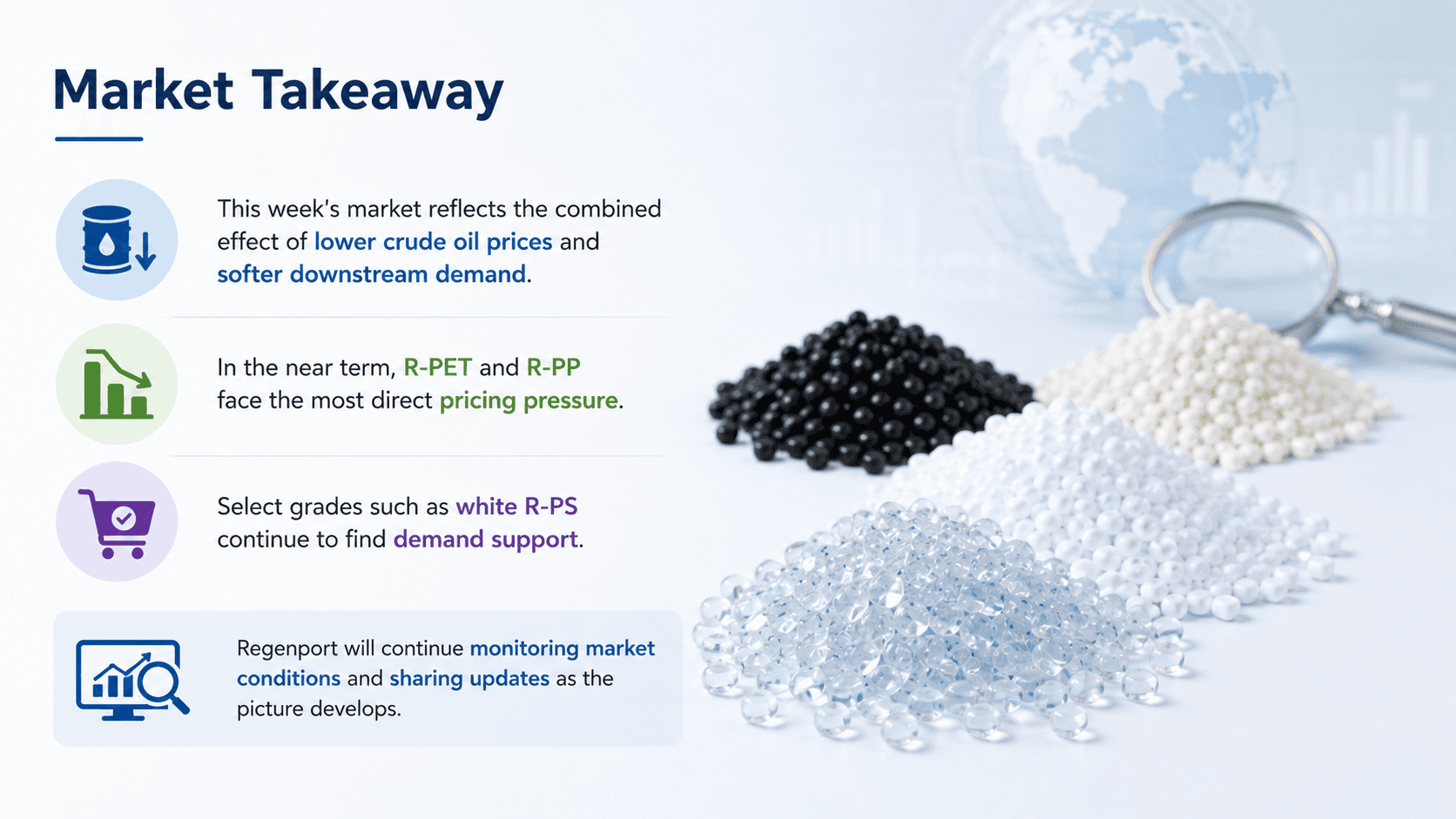

Market takeaway

This week's market reflects the combined effect of lower crude oil prices and softer downstream demand. In the near term, R-PET and R-PP face the most direct pricing pressure, while select grades such as white R-PS continue to find demand support. Regenport will continue monitoring market conditions and sharing updates as the picture develops.

Image generated with ChatGPT

The recycled polymer market remained under pressure this week, shaped by three converging factors: lower crude oil prices amid US–Iran peace deal expectations, seasonal demand softness in Europe, and rising shipping costs out of Asia. Together, these trends have made buyers more cautious and reduced appetite for recycled feedstock across key grades.

Three Factors Driving Market Pressure

Crude oil and virgin polymer prices

Expectations of a US–Iran peace agreement pushed Brent crude below 80 USD per barrel this week, pulling virgin polymer prices lower in tandem. As the price gap between virgin and recycled materials narrows, some buyers have begun shifting their procurement mix toward virgin feedstock, reducing near-term demand for recycled alternatives.

Seasonal slowdown in Europe

Purchasing activity in Europe is easing as the market approaches the summer holiday period. Export flows from Asia to European converters have also softened, adding to the overall demand slowdown across the region.

Rising freight costs

Shipping rates out of Asia have roughly doubled since April, creating an additional barrier to cross-border cargo movement. For recycled polymer trades that depend on longer supply chains, the economics of importing have become more challenging.

Key Grade Performance: R-PET, R-PP, and R-PS

rPET Market

Demand for R-PET continued to soften this week. Thermoformers and converters have adjusted their procurement mix toward virgin feedstock in some cases, and several recyclers noted that rPET demand has returned to pre-conflict levels — reflecting how much of the recent demand strength was tied to the period of US–Iran tensions.

In Europe, flake and pellet prices fell by EUR 10 to EUR 20 per metric ton. In the United States, overall fundamentals remained sluggish, although bale demand held relatively stable, supported by steady purchases from Mexico.

rPP Market

European R-PP prices came under seasonal pressure as agricultural sector demand moves toward its seasonal close. Black pellets declined by EUR 10 per metric ton, while natural pellets fell by EUR 30 per metric ton.

rPS Market

R-PS showed relative resilience despite the broader pressure from lower virgin prices. White pellet prices rose by EUR 20 per metric ton on stronger demand, while black pellets remained broadly stable — a reminder that grade-specific demand dynamics can diverge meaningfully from the broader market trend.

Key company updates

Hanwha Solutions reduced its PVC operating rates to around 60–70% this week. LyondellBasell officially confirmed it will permanently shut its remaining PP plant in Brindisi, Italy — capacity of 260,000 metric tons per year — by the end of 2026. Formosa Chemical & Fibre Corp. restarted its 1.5 million metric ton per year PTA plant in Ningbo, China, following a scheduled turnaround that began in May.

Market takeaway

This week's market reflects the combined effect of lower crude oil prices and softer downstream demand. In the near term, R-PET and R-PP face the most direct pricing pressure, while select grades such as white R-PS continue to find demand support. Regenport will continue monitoring market conditions and sharing updates as the picture develops.

Image generated with ChatGPT

Looking for samples or ready to source? Submit your request for pricing, availability, and technical information.

Looking for samples or ready to source? Submit your request for pricing, availability, and technical information.

Request a Quote →

Request a Quote →

Samples • Pricing • Availability

Request a Quote →

Posted by REGENPORT

REGENPORT is a global platform connecting buyers and suppliers in the recycled materials and sustainable packaging industries.